Capital Mobility and Stabilization Policy under Fixed and Flexible Exchange Rates

Robert A. Mundell

The world is still a closed economy, but its regions and countries are becoming increasingly open. The trend, manifested in both freer movement of goods and increased mobility of capital, has been stimulated by the dismantling of trade and exchange controls in Europe, the gradual erosion of the real burden of tariff protection, and the stability, unparalleled since 1914, of the exchange rates. The international economic climate has changed in the direction of financial integration and this has important implications for economic policy.

My paper concerns the theoretical and practical implications of the increased mobility of capital. To present my conclusions in the simplest possible way, and to bring the implications for policy into sharpest relief, I assume the extreme degree of mobility that prevails when a country cannot maintain an interest rate different from the general level prevailing abroad. This assumption will overstate the case, but it has the merit of posing a stereotype toward which international financial relations seem to be heading. At the same time it might be argued that the assumption is not far from the truth in those financial centers of which Zurich, Amsterdam, and Brussels may be taken as examples, where the authorities already recognize their lessening ability to dominate money market conditions and insulate them from foreign influences. It should also have a high degree of relevance to a country like Canada, whose financial markets are dominated to a great degree by the vast New York market.

Sectoral and Market Equilibrium Conditions

The assumption of perfect capital mobility can be taken to mean that all securities in the system are perfect substitutes. Because different currencies are involved, this implies that existing exchange rates are expected to persist indefinitely (even when the exchange rate is not pegged) and that spot and forward exchange rates are identical. All the complications associated with speculation, the forward market, and exchange-rate margins are thereby assumed not to exist.

To focus attention on policies affecting the level of employment, we assume unemployed resources, constant returns to scale, and fixed money wage rates; this means that the supply of domestic output is elastic and its price level constant. We assume further that saving and taxes rise with income, that the balance of trade depends only on income and the exchange rate, that investment depends on the rate of interest, and that the demand for money depends only on income and the rate of interest. Our last assumption is that the country under consideration is too small to influence foreign incomes or the world level of interest rates.

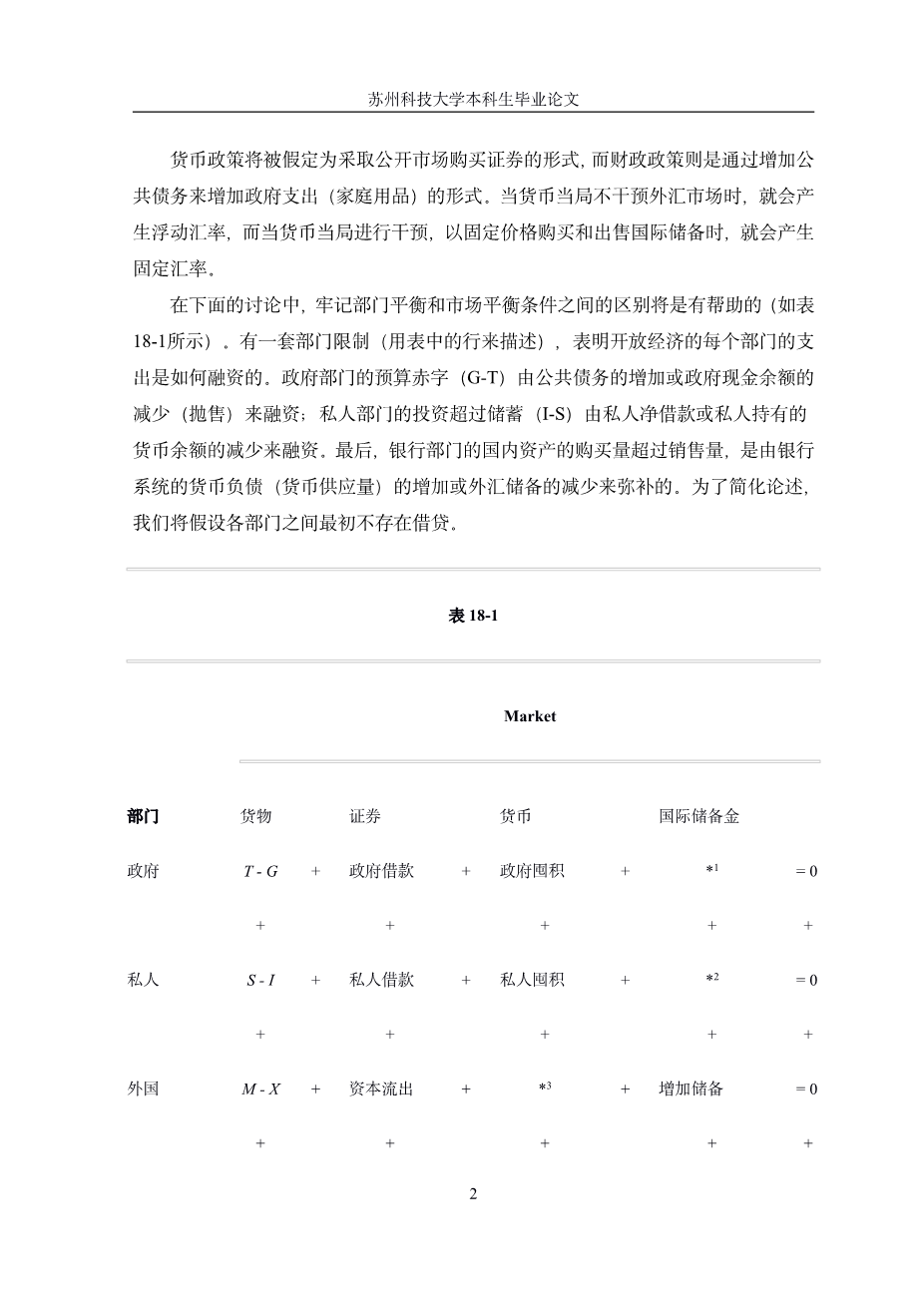

Monetary policy will be assumed to take the form of open market purchases of securities, and fiscal policy the form of an increase in government spending (on home goods) financed by an increase in the public debt. Floating exchange rates result when the monetary authorities do not intervene in the exchange market, and fixed exchange rates when they intervene to buy and sell international reserves at a fixed price.

It will be helpful, in the following discussion, to bear in mind the distinction between conditions of sectoral and market equilibria (illustrated in Table 18-1). There is a set of sectoral restraints (described by the rows in the table) that show how expenditure in each sector of the open-economy is financed: A budget deficit (G - T) in the government sector is financed by an increase in the public debt or a reduction in government cash balances (dishoarding); an excess of investment over saving (I - S) in the private sector is financed by net private borrowing or a reduction in privately held money balances; a trade balance deficit (M - X) in the foreign sector3 is financed by capital imports or a reduction in international reserves; and, finally, an excess of purchases over sales of domestic assets of the banking sector is financed by an increase in the monetary liabilities of the banking system (the money supply) or by a reduction in foreign exchange reserves. For simplicity of exposition, we shall assume that there is, initially, no lending between the sectors.

<t

剩余内容已隐藏,支付完成后下载完整资料</t

英语译文共 24 页,剩余内容已隐藏,支付完成后下载完整资料

资料编号:[587440],资料为PDF文档或Word文档,PDF文档可免费转换为Word

|

Table 18-1 |

||||||||

|

Market |

||||||||

|

Sector |

Goods |

Securities |

Money |

International |

||||

|

Government |

T - G |

|

Government |

|

Government |

|

*1 |

= 0 |

|

|

|

|

|

|

||||

|

Private |

S - I |

|

Private |

|

Private |

|

*2 |

= 0 |

|

|

|

|

|

|

||||

|

Foreign |

M - X |

|

Capital |

|

*3 |

|

Increase |

= 0 |

|

|

|

|

|

|

||||

|

Banking |

*4 |

|

||||||

课题毕业论文、文献综述、任务书、外文翻译、程序设计、图纸设计等资料可联系客服协助查找。